You may wonder, should you get an LLC for rental property in Florida when you face risks like tenant lawsuits, storms, or repair claims? An LLC gives liability protection by separating personal assets, and you form one in Florida by filing Articles of Organization on Sunbiz.org with the Florida Division of Corporations.

This post will explain LLC landlord benefits, tax advantages like pass-through taxation, and steps such as an operating agreement, insurance updates, and separate records. Keep reading.

Key Takeaways

- Forming an LLC for rental property in Florida protects your personal assets from lawsuits and claims. It keeps your home and savings safe if legal issues arise with tenants or repairs.

- An LLC offers tax benefits. You can use pass-through taxation, deduct business expenses like repairs, insurance, and management fees, and speed up depreciation to lower your taxes.

- Starting an LLC in Florida costs at least $125 to file on Sunbiz.org. Annual franchise taxes range from $250 to $800. Other costs include legal fees, new loan requirements, title transfer tax ($0.70 per $100 value), and possible higher mortgage rates.

- Managing a rental property through an LLC requires you to keep separate bank accounts and financial records. You should update your insurance policies to name the LLC as the owner for full protection.

- Some banks may refuse loans or require extra steps when you move a property into an LLC because of due-on-sale clauses. Always check with lenders before transferring ownership to avoid problems.

What Is an LLC?

A limited liability company, or limited liability company, separates personal assets from business liabilities for landlords and property owners. Florida LLCs follow Florida Statutes, Chapter 605, and must include the designation, LLC, or Limited Liability Company, in the official name.

Owners form an LLC by filing Articles of Organization with the Florida Division of Corporations, Sunbiz.org, and they should adopt an operating agreement to set roles.

An LLC acts as a pass-through entity, so the Internal Revenue Service lets owners report rental income on personal returns, which ties to tax advantages of LLC for rental property.

An LLC can have one or multiple owners, and it requires a separate business bank account to keep finances distinct. Landlords gain asset protection and easier estate planning, but owners should weigh llc pros and cons for rental property before deciding.

Reasons to Use an LLC for Rental Property in Florida

Florida landlords often form LLCs to help manage real estate risk and stay private. This choice can also simplify passing property to family in the future—keep reading for deeper insights on how groups like Allegiant Management Group or The Law Offices of Kate Mesic, P.A.

might guide you through local rules.

Liability Protection

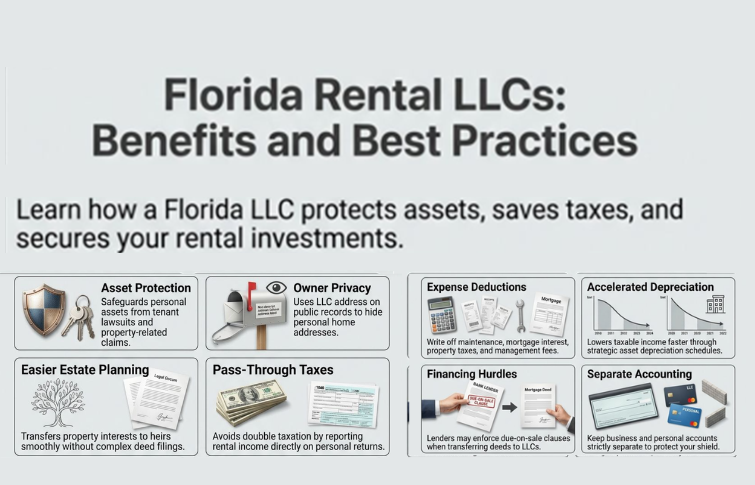

Using an LLC for rental property offers strong liability protection. This means your personal assets are safer from lawsuits tied to your rental activities. If a tenant has issues, they can only target the LLC’s assets, not your home or savings.

Each property can be placed in its own LLC. This way, problems with one property won’t affect the others.

To maintain this protection, keep business and personal finances separate. Mixing them can weaken your shield against legal claims. A clear operating agreement is vital if multiple owners hold properties together; it helps outline everyone’s rights and duties.

Using an umbrella insurance policy alongside an LLC adds another layer of safety for landlords.

Liability protection is strongest when you keep business and personal finances separate.

Privacy for Property Owners

An LLC can provide privacy for property owners in Florida. Forming one allows you to use the property address instead of your personal address in public records. This keeps your home and personal life safer from prying eyes.

The state keeps ownership records of an LLC, which means not all details about you will be public. By naming the LLC after the property’s address, like “123 Main Street LLC,” you boost both privacy and uniqueness.

Ownership interests can also be transferred without filing a public deed, further protecting your information as a landlord while managing rental properties effectively.

Simplified Estate Planning

Using an LLC for rental property makes estate planning easier. Rental properties owned by an LLC can be passed to family members without complex legal steps. This allows for smooth ownership transitions, saving families time and money.

Owners can transfer interests instead of deeds, which simplifies the process.

LLCs also help with tax bills during transfers. Property owners can use annual gift tax exclusions to give their property gradually to heirs. This lowers estate taxes too. Having an operating agreement in place means that succession plans are clear; it outlines how properties will be inherited by future generations, making things less stressful for everyone involved in real estate investing.

Tax Benefits of an LLC for Rental Property

An LLC can help you save on taxes for your rental property. It allows you to use pass-through taxation, meaning the income goes directly to you without double taxation. You can also deduct business expenses like repairs and management costs.

Plus, there are ways to speed up depreciation deductions, which lowers your taxable income even more. Curious about all the benefits? There’s a lot more to explore!

Pass-Through Taxation

Pass-through taxation is an important benefit of using an LLC for rental property. It means the income from the property goes directly to the owners, skipping double taxation. Instead of paying taxes at both the business and personal levels, owners report rental income on their own tax returns.

This approach minimizes tax burdens and simplifies how landlords file taxes. Most times, LLCs are treated as pass-through entities by default.

For single-member LLCs, this process usually makes filing easier. Income is taxed only once at the member level. Multi-member LLCs also enjoy this status but must file an informational partnership return for reporting purposes.

Rental profits and losses flow directly to each owner’s individual return. Owners can take advantage of benefits such as deducting business expenses or utilizing accelerated depreciation deductions too, making it a smart choice for many investors in real estate law like Florida’s market.

Deductible Business Expenses

Choosing an LLC for rental properties can bring several tax advantages. Landlords can save money by deducting certain expenses associated with their rental activity.

- Maintenance and Repairs: Costs for fixing issues in your property are deductible. This includes plumbing, electrical work, or any other needed repairs.

- Mortgage Interest: The interest on loans used to buy property qualifies as a business expense. This deduction can lower your taxable income significantly.

- Property Taxes: You can deduct taxes paid to the local government on your rental property. This lowers your overall property tax burden.

- Insurance Premiums: Expenses for landowner insurance are deductible as well. This includes liability insurance and property insurance costs.

- Supplies: Any supplies needed for managing the property can be deducted. Think of cleaning supplies or maintenance tools that help keep the place in good shape.

- Professional Fees: Legal fees, contracting expenses, and fees paid to real estate agents are also deductible. They directly relate to managing your rental business.

- Management Costs: If you hire a property management company, their fees can be deducted too. This helps cover the cost of professional services while you focus on other things.

- Business Bank Accounts: Keeping financial records separate makes tracking easier, enabling better expense management and clearer deductions related to your rentals.

Tracking these deductions is essential for maximizing savings and ensuring smooth operations in Florida’s property market.

Accelerated Depreciation Deductions

Accelerated depreciation deductions help lower tax bills for rental property owners. LLCs allow landlords to take these deductions each year, reducing their taxable income over time.

This method speeds up the process compared to ownership as an individual. Owners can use cost segregation studies within LLCs to break down property values further. Doing so increases cash flow and boosts the investment value.

Landlords benefit from clearer depreciation schedules when properties are held in an LLC. These deductions show on the owner’s tax return due to pass-through taxation. The savings from accelerated depreciation are especially valuable for those owning multiple properties, like members of groups such as the National Association of Realtors or investors using a qualified business income deduction strategy.

Challenges of Using an LLC for Rental Property

Using an LLC for rental property can bring some challenges. Financing might be tougher, as banks often worry about lending to an LLC. The costs of setting up and maintaining the LLC can also be significant.

Financing Limitations

Financing a rental property through an LLC can be tricky. Most mortgages have a due-on-sale clause. This means lenders may demand full repayment if you transfer the property to an LLC.

If not disclosed, the clause could lead to loan default. Many lenders also require prior approval before allowing any transfer into your new LLC.

Some institutions do not permit transfers at all. They may instead ask for a new loan, which complicates things further for owners looking to protect their assets with an LLC. You might face higher interest rates or extra fees when seeking these approvals too.

Always make sure title and mortgage names match; otherwise, it can hurt your rights during foreclosure proceedings as well.

Setup and Maintenance Costs

Registering and running a Florida rental LLC carries clear setup and ongoing costs.

| Cost Item | Typical Range | Notes |

|---|---|---|

| LLC filing fee, Articles of Organization | $125 | File via Sunbiz.org, one-time state filing. |

| Annual franchise tax | $250 to $800 | State assessed yearly, varies by filings and revenues. |

| Annual maintenance fees | $9 to $500 | Covers reports, registrations, and routine filings. |

| Title transfer tax | $0.70 per $100 of value | May apply twice if an existing mortgage must be cleared or reassigned. |

| Quitclaim deed filing | $10 to $50 | Used to move title into the LLC, cost varies by county. |

| Operating agreement | $0 to $1,000 | DIY is free, attorney drafting raises cost. |

| Notice of intent to form (if required) | About $40 | Local publication fees, check county rules. |

| Mortgage and financing impacts | Potential for higher rates | Mortgage may need lender consent; rates can rise after transfer. |

| Property tax reassessment | Varies by county | Title transfer can trigger reassessment and higher taxes. |

| Legal and professional fees | Varies | Includes attorney, CPA, and title company charges. |

| Other transactional costs | Varies | Recording fees, courier charges, and minor county fees. |

Best Practices for Managing a Rental Property LLC

Managing a rental property LLC can be simple if you follow some key practices. Keep your money matters separate from personal funds to avoid confusion. Get the right insurance to protect your assets, and consult with experts like lawyers or accountants for guidance.

In Orlando, a property management company like Guest Managers can guide you in getting an LLC by coordinating with the right experts for LLC setup, in addition to providing full-stack, worry-free management of your property.

This way, you reduce risks and make smart decisions….

Keep Financial Records Separate

Keeping separate financial records is essential for any rental property LLC. This practice protects your personal assets and ensures proper tax deductions.

- Open a separate bank account for the LLC. This keeps business funds away from personal money, making tracking easier.

- Use distinct credit cards for business purchases. It prevents mix-ups with personal expenses and simplifies record-keeping.

- Maintain detailed financial records. Detailed records support liability protection and help in taking advantage of tax benefits.

- Log all rent payments and fees automatically through tools like Avail. This creates a clear overview of cash flow and saves time.

- Include repair costs and vendor fees in accounting reports. Tracking these costs helps landlords manage budgets effectively.

- Generate customized reports regularly, detailing payments, late fees, maintenance tasks, and lease expirations. This aids in clear management of the property.

- Keep all documents organized for tax filings and compliance checks with the Florida Department of State. Proper organization ensures you can respond quickly to any inquiries or audits.

Following these steps can strengthen your rental property LLC’s financial health while protecting your investment from risks like documentary stamp tax issues or breaches of the corporate veil.

Obtain Adequate Insurance

Landlords need to obtain adequate insurance for their rental properties. It’s not enough to rely on LLC liability protections alone. Landlord-specific insurance policies cover unique risks related to rentals.

This includes property damage, natural disasters, and tenant-related issues.

Insurance must show LLC ownership. If it does not, claims may get denied. Landlords should also consider umbrella coverage for extra protection, especially if they own one or two properties.

Regularly review and update these policies as new properties are added or removed from the LLC. For those with multiple homes, tailor each policy to fit its needs; different structures require different coverage amounts.

Consult With Professionals

Consulting with professionals is key for rental property LLCs. A Florida real estate attorney, can help you move your property into an LLC. They guide you through legal steps like drafting Articles of Organization and creating an operating agreement.

This support is crucial to avoid errors that could lead to penalties.

Tax experts, such as CPAs, also play a big role. They can uncover additional deductions and credits specific to rental properties. Proper guidance ensures compliance with annual reports and renewal fees.

Always seek advice before making big decisions about your LLC structure or financing options; it saves time and money in the long run.

Conclusion

Getting an LLC for rental property in Florida offers many benefits. It protects your assets and gives you privacy as a landlord. You can enjoy tax advantages, too. However, some challenges come with it, like costs and financing issues.

Weigh these factors carefully to make the best choice for your rentals. Let Guest Managers provide guidance when it comes to getting an LLC for your rental property in Florida while also taking care of your property’s day-to-day management. Contact us today and make your rental investment truly worry-free.

FAQs

1. Do I need an LLC for rental property in Florida?

No, you do not need an LLC. A limited liability company can shield your personal assets from rental claims. It can help with legal separation between you and the property. Note, homestead exemption usually applies only to your main home. Moving a residence into an LLC can end that exemption.

2. What benefits does an LLC give a property owner in Florida?

An LLC gives strong liability protection. It helps keep renter claims off your personal accounts. It can make sale and transfer simpler. Always get title insurance when you change ownership, to protect against hidden title problems.

3. Are there tax or filing rules I must know about?

Yes. An LLC can elect s corp status in some cases, to change how taxes are paid. Check if that helps your situation, talk to a tax pro. Also, new boi reporting rules can require you to file who really owns the company. Forbes has clear guides on these topics, read them for context.

4. What steps should I take before I move a rental into an LLC?

Check if you will lose the homestead exemption. Get title insurance for any deed change. Talk to an attorney and an accountant. Prepare for boi reporting and other filings. Keep clear records, and pick the right entity type for your goals.